The debt-to-equity ratio (D/E) compares the total debt balance on a company’s balance sheet to the value of its total shareholders’ equity. When using a real-world debt to equity ratio formula, you’ll probably be able to find figures for both total liabilities and shareholder equity on a company’s fathom vs dryrun balance sheet. Publicly traded companies will usually share their balance sheet along with their regular filings with the Securities and Exchange Commission (SEC). Common debt ratios include debt-to-equity, debt-to-assets, long-term debt-to-assets, and leverage and gearing ratios.

What does a negative D/E ratio mean?

In summary, computing the Debt to Equity ratio is essential for assessing financial health and risk. Companies should regularly evaluate their ratio to ensure it aligns with their strategic goals. Debt ratio on its own doesn’t provide insights into a company’s operating income or its ability to service its debt.

What Does a Negative D/E Ratio Signal?

The following D/E ratio calculation is for Restoration Hardware (RH) and is based on its 10-K filing for the financial year ending on January 29, 2022. Of note, there is no “ideal” D/E ratio, though investors generally like it to be below about 2. It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, and more.

- The principal payment and interest expense are also fixed and known, supposing that the loan is paid back at a consistent rate.

- For example, a company may not borrow any funds to support business operations, not because it doesn’t need to but because it doesn’t have enough capital to repay it promptly.

- The investor has not accounted for the fact that the utility company receives a consistent and durable stream of income, so is likely able to afford its debt.

- On the other hand, a comparatively low D/E ratio may indicate that the company is not taking full advantage of the growth that can be accessed via debt.

- The debt-to-equity (D/E) ratio can help investors identify highly leveraged companies that may pose risks during business downturns.

Putting the D/E in Context

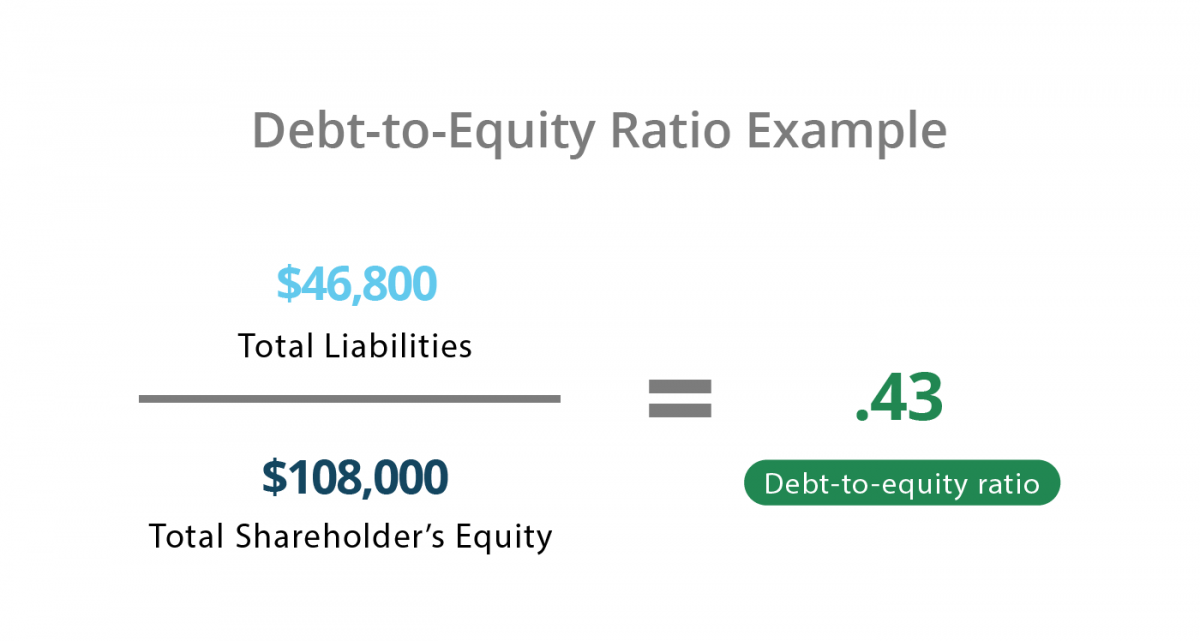

Put another way, if a company was liquidated and all of its debts were paid off, the remaining cash would be the total shareholders’ equity. In most cases, liabilities are classified as short-term, long-term, and other liabilities. The ratio looks at debt in relation to equity, providing insights into how much debt a company is using to finance its operations. For growing companies, the D/E ratio indicates how much of the company’s growth is fueled by debt, which investors can then use as a risk measurement tool. The debt-to-equity (D/E) ratio is a metric that shows how much debt, relative to equity, a company is using to finance its operations.

What is considered a high ratio can depend on a variety of factors, including the company’s industry. This ratio, calculated by dividing total liabilities by total assets, serves as a valuable tool for assessing a company’s financial stability, gauging risk exposure, and evaluating capital structure. The debt-to-equity ratio is calculated by dividing total liabilities by shareholders’ equity or capital. Acceptable levels of the total debt service ratio range from the mid-30s to the low-40s in percentage terms. Last, businesses in the same industry can be contrasted using their debt ratios. It offers a comparison point to determine whether a company’s debt levels are higher or lower than those of its competitors.

A company may be at or below the industry average but above its own historical average, which can be a cause for concern. In this case, it is important to analyze the company’s current situation and the reasons for the additional debt. At the very least, a company with a high amount of debt may have difficulty paying or maintaining dividend payments for investors. Debt ratio provides insights into a company’s capital structure by showcasing the balance between debt and equity. From the perspective of companies, it is therefore important to measure the debt-to-equity ratio because capital structure is one of the fundamental considerations in financial management.

That’s because share buybacks are usually counted as risk, since they reduce the value of stockholder equity. As a result the equity side of the equation looks smaller and the debt side appears bigger. Ultimately, businesses must strike an appropriate balance within their industry between financing with debt and financing with equity.

By contrast, higher D/E ratios imply the company’s operations depend more on debt capital – which means creditors have greater claims on the assets of the company in a liquidation scenario. Lenders and debt investors prefer lower D/E ratios as that implies there is less reliance on debt financing to fund operations – i.e. working capital requirements such as the purchase of inventory. A D/E ratio of about 1.0 to 2.0 is considered good, depending on other factors like the industry the company is in. But a D/E ratio above 2.0 — i.e., more than $2 of debt for every dollar of equity — could be a red flag. Again, context is everything and the D/E ratio is only one indicator of a company’s health. A company’s accounting policies can change the calculation of its debt-to-equity.

Debt-to-Equity Ratio, often referred to as Gearing Ratio, is the proportion of debt financing in an organization relative to its equity. For example, utilities tend to be a highly indebted industry whereas energy was the lowest in the first quarter of 2024. Inflation can erode the real value of debt, potentially making a company appear less leveraged than it actually is. It’s crucial to consider the economic environment when interpreting the ratio.

On the other hand, the typically steady preferred dividend, par value, and liquidation rights make preferred shares look more like debt. The debt ratio focuses exclusively on the relationship between total debt and total assets. However, companies might have other significant non-debt liabilities, such as pension obligations or lease commitments. Newer businesses or startups might rely heavily on debt financing to kick-start operations, leading to higher debt ratios. Debt-to-equity ratio of 0.20 calculated using formula 3 in the above example means that the long-term debts represent 20% of the organization’s total long-term finances.